Question # 4

Jelena, age 32, is single and works as a partner in a law firm. She is meeting with her financial planner, May, as she would like to start investing. Her friend John talks about hot sectors in the stock markets and has recently brought up the cannabis sector. She has done some reading about this sector and is willing to experience large decline in her investments. Jelena also mentioned to May that she believes in high long-term returns. What conclusion can May draw based on their discussions about the stock market and Jelena's expectations?

Question # 5

The Andersons, a young couple, meet with their financial planner to review estate-planning opportunities. They recently had a third child and are looking for the most cost-effective strategy to put in place during their working years to increase their estate value and reduce the tax burden at death for the benefit of their children. What should the financial planner recommend?

Question # 6

William and Jennifer are selling their business which qualifies as a Canadian-controlled private corporation. When the sale is complete at the end of this year, William and Jennifer will each receive $4 million for their common shares which have nominal cost. Jennifer has unused capital losses from previous years. They are meeting with Laurel, their financial planner, to discuss the tax implications of the sale. Based on the information provided, what should Laurel recommend to William and Jennifer so that they are best able to make use of the Lifetime Capital Gains Exemption?

Question # 7

A retiree receives income-tested benefits and needs occasional withdrawals for vacations and home repairs. Which account is generally most efficient for withdrawals that do not increase taxable income?

Question # 8

Ram Patel, age 65, is meeting with his financial planner, Maria Romano, to complete a financial plan. Ram is retiring this year, and his company provides a defined benefit pension plan. Upon retirement, he has the choice of receiving $20,000 each year for 20 years or until death (whichever is earlier), or he can take $304,300, which is the commuted value at retirement. Ram has confirmed that he will be transferring the commuted value to a LIRA. After further discovery, Maria suggests that they utilize a 5% market rate of return and project the funds to last 25 years. What should Maria update Ram's projected annual retirement income to?

Question # 9

Richard reviewed his divorce settlement from his partner Alex with his advisor Maria. He is deciding between providing a lump sum spousal support payment of $60,000 or making monthly payments. If Richard’s income is $200,000 and Alex’s income is $40,000, what should Maria advise Richard about the tax implications for both Richard and Alex in regard to the lump sum payment?

Question # 10

Alexis has an index-linked GIC with an adjusted cost base of $20,500. The GIC was issued one year ago, has four years remaining to maturity and provides her with 60% participation in the gains of the S & P/TSX 60 Index, based on the level of the Index at maturity or at redemption prior to maturity. The GIC has a 2% fee if redeemed in the first two years. Alexis notices that the S & P/TSX 60 Index is up 25% and she would like to redeem her GIC. She asked her financial planner if she redeems her GIC, how much she would receive upon redemption. What will her financial planner tell her?

Question # 11

Edward is risk averse and has limited investment knowledge. He will only purchase 100% guaranteed products insured by the CDIC. Edward is meeting with his financial planner, Marissa, for the third time this year about rates, and starts the meeting by criticizing her employer for paying such low returns on GICs. Edward says he is considering taking his business elsewhere. How should Marissa respond to Edward’s comments?

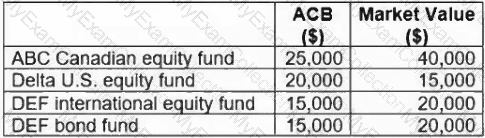

Question # 12

Janet's non-registered account holds the funds listed in the following table:

Assuming a marginal tax rate of 45%, what amount of tax payable will Janet incur if she redeems the account to fund the purchase of a new business?

Question # 13

A married couple has a $480,000 mortgage with 15 years remaining. They want the mortgage retired if either spouse dies during that period. What insurance structure best fits this objective?

Question # 14

Richard pays periodic spousal support and child support under a written separation agreement. Which statement is generally correct?

Question # 15

A retiree holds most of her investments in interest-bearing GICs inside a non-registered account while her TFSA is invested in cash. She has unused TFSA room and wants to improve after-tax efficiency without increasing total portfolio risk materially. What should the planner consider?

Question # 16

Robert is meeting with his wealth advisor to review options to put a plan in place to save for his children's education. He has a daughter, age seven, and a disabled son, age four Robert would like to maximize his savings towards this goal, ensure the strategy is tax efficient and utilize available grants. Which option is most appropriate for Robert's plan?

Question # 17

Priya grants her brother trading authority over her non-registered investment account. Her brother calls the financial planner and asks for Priya’s full net worth statement, tax return, and beneficiary information so he can “help with planning.†What should the planner do?

Question # 18

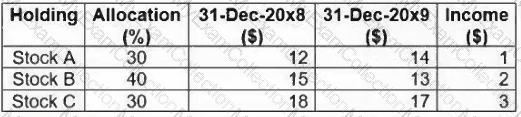

Consider the following information for a client's portfolio:

What is the annual rate of return for this portfolio?

Question # 19

A financial planner, Rachel, is preparing to recommend a discretionary portfolio manager to her client. The portfolio manager is owned by Rachel’s former employer, and Rachel receives no referral fee. However, the former employer regularly sends new clients to Rachel’s practice. What should Rachel do before making the recommendation?

Question # 20

Alexander and Irena, age 30 and 32 respectively, are married and have been working full-time for one year. They have a daughter, age 3, and are expecting their second child. They recently bought a home with a mortgage balance of $390,000 at 4% amortized over 25 years. Their financial planner is trying to determine their tolerance for risk. After completing the life-cycle analysis, how can their financial planner explain the stage in which the couple finds themselves and the risk tolerance associated with it?

Question # 21

If a deceased person was entitled to rights or things at death, what strategy should the estate representative use to enhance the net estate value after tax?

Question # 22

Two shareholders sign a buy-sell agreement requiring the surviving shareholder to purchase the deceased shareholder’s shares at fair market value. What planning tool most directly funds the death-triggered purchase obligation?

Question # 23

Huxley is meeting with his financial planner to review his retirement goals. He has saved $250,000 in an RRSP, currently contributes $10,000 per year, and his portfolio is expected to continue to earn an average of 5% per year. Huxley is hoping to retire in 18 years with $1 million saved in his RRSP. What strategy should Huxley's financial planner recommend to ensure he is on track?

Question # 24

A financial planner is invited to serve as a paid director of a private corporation owned by one of her clients. The client also wants the planner to continue providing personal financial planning advice. What should the planner do before accepting the directorship?

Question # 25

Ronny, a successful business owner, established a discretionary family trust earlier this year as a means to split income with his children. Ronny's children are both under the age of five and are both income and capital beneficiaries of the trust. He is concerned that the 21-year rule will result in a significant amount of tax resulting from unrealized capital gains. What strategy would be best if Ronny's goal is to minimize the total amount of tax payable by the trust and/or beneficiaries at the 21-year mark?

Question # 26

Rosa has just learned that her daughter Marissa, age 23, does not intend to return to university. She has been saving for her daughter's education since Marissa was 10 and is concerned there will be a significant tax liability. How should Rosa's financial planner advise her to utilize the funds when she redeems the RESP in order to offset the tax liability?

Question # 27

Todd, a financial planner, is meeting with Vanessa, a new client, to review her investment goals and objectives. During the meeting, Vanessa states that she believes the markets are very efficient and should reflect all available information in the price of securities. She is looking for an investment option that will reflect a similar level of risk and return characteristics as the Canadian market. What investment option should Todd recommend with Vanessa that would reflect her opinions?

Question # 28

Henri and Jessica have recently moved in together and Henri has been helping Jessica with her investments. Jessica names Henri trading authority on her TFSA. Henri calls their financial planner requesting to make Jessica's TFSA contribution for this year but first requests the overall balance in Jessica's bank accounts (TFSA, high yield savings, chequing) to know if this is possible. What action would be most appropriate for their financial planner to take?

Question # 29

Henry, age 48, has been working for Bac Inc, which is a federally regulated corporation, for over eight years. He is looking to retire at age 50 and has decided to take the commuted value of his pension: $450,000, electing to transfer the eligible remainder to his RRSP (Income Tax Act maximum pension benefit transfer value of $210,000). Henry estimates he would need $1,800 (pre-tax every month) from his registered investments to meet his retirement income goal and is looking to maximize his RRSP contribution room. Assume no inflation, an average tax rate of 15%, an unused RRSP contribution room of $90,000, and a life expectancy to age 90. What would be the required rate of return to meet Henry's goals?

Question # 30

Dianna has just taken a 20-year mortgage and wants insurance only to ensure the mortgage can be repaid if she dies during that period. She is considering whole life insurance. What should her planner most likely explain?

Question # 31

Sarah Jones is an incorporated owner of a successful manufacturing company. She currently has a large month to month cash flow surplus. This is expected to continue until she retires in seven years. Her personal mortgage is up for renewal. She needs to borrow $50,000 so that she can replace a piece of equipment that is needed in the manufacturing process. She would like a solution that results in paying the lowest interest cost over the life of the loan. Which loan product should the financial planner recommend to Sarah? Assume monthly compounding for all products and no pre-payment options.

Question # 32

What key question should be answered during the recommending strategies stage of the financial planning process?

Question # 33

In which life cycle stage would a financial planner identify his client to be if they have a high mortgage balance and an unstable or lower income, and are willing to take on investment risk because of their longer time horizon?

Question # 34

Dianna is visiting with Karen, her Financial Planner, and is excited to report that she has just bought her dream home. She has also let Karen know she Is meeting with an insurance representative to purchase a whole life insurance to cover her 20-year mortgage. Why might Karen suggest Dianna consider term life insurance instead?

Question # 35

Keitaro wants his spouse to receive income from his assets for life after his death, but wants the remaining capital to pass to his children from a prior marriage after the spouse dies. Which strategy best fits this objective?