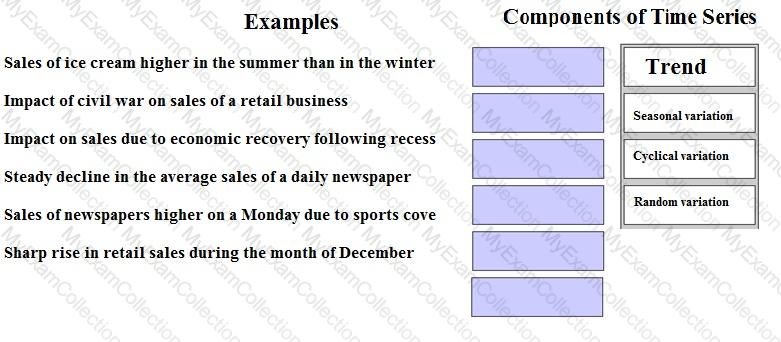

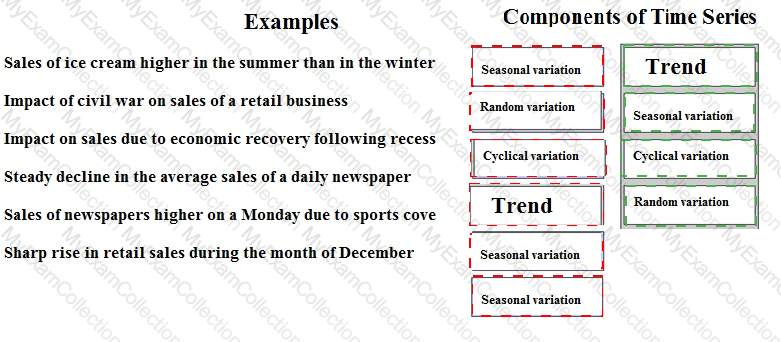

Question # 5

Place the components of the time series next to the example about the impact on sales that they best represent.

Question # 6

A company is bidding to win a special contract.

Which of the following is NOT a relevant cost to the company of undertaking the contract?

Question # 7

The simplex method has been used to determine the optimum output of products P, Q, R and S with constraints on resources J, K and L.

In the final simplex tableau, the figure in the product R row and the column for slack variable K is 80.

Which of the following statements is correct?

Question # 8

RFT, an engineering company, has been asked to provide a quotation for a contract to build a new engine. The potential customer is not a current customer of RFT, but the directors of RFT are keen to try and win the contract as they believe that this may lead to more contracts in the future. As a result, they intend pricing the contract using relevant costs. The following information has been obtained from a two-hour meeting that the Production Director of RFT had with the potential customer. The Production Director is paid an annual salary equivalent to $1,200 per 8-hour day. 110 square meters of material A will be required. This is a material that is regularly used by RFT and there are 200 square meters currently in inventory. These were bought at a cost of $12 per square meter. They have a resale value of $10.50 per square meter and their current replacement cost is $12.50 per square meter. 30 liters of material B will be required. This material will have to be purchased for the contract because it is not otherwise used by RFT. The minimum order quantity from the supplier is 40 liters at a cost of $9 per liter. RFT does not expect to have any use for any of this material that remains after this contract is completed. 60 components will be required. These will be purchased from HY. The purchase price is $50 per component. A total of 235 direct labour hours will be required. The current wage rate for the appropriate grade of direct labour is $11 per hour. Currently RFT has 75 direct labour hours of spare capacity at this grade that is being paid under a guaranteed wage agreement. The additional hours would need to be obtained by either (i) overtime at a total cost of $14 per hour; or (ii) recruiting temporary staff at a cost of $12 per hour. However, if temporary staff are used they will not be as experienced as RFT’s existing workers and will require 10 hours supervision by an existing supervisor who would be paid overtime at a cost of $18 per hour for this work. 25 machine hours will be required. The machine to be used is already leased for a weekly leasing cost of $600. It has a capacity of 40 hours per week. The machine has sufficient available capacity for the contract to be completed. The variable running cost of the machine is $7 per hour. The company absorbs its fixed overhead costs using an absorption rate of $20 per direct labour hour.

Select ALL the true statements.

Question # 9

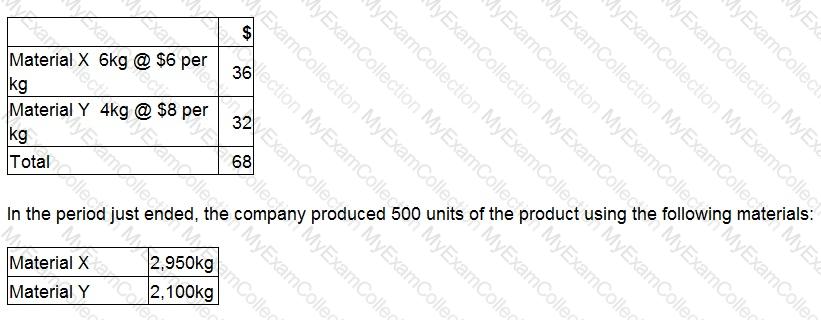

A company makes a product using two materials, X and Y.

The standard materials required for one unit of the product are:

What is the materials yield variance?

Give your answer as a whole number.

Question # 10

A snowboard manufacturer is considering investing in technology that will give a good indication of how heavy snowfall will be in the future. The predictions tend to be reasonably accurate.

The current budgeted profit for the year is £2,560,000 but if they invest in this technology and it works, the expected profit will be £2,640,000. The manufacturer is willing to invest a maximum of £40,000 into the venture.

What is the expected profit if the investment is NOT made?

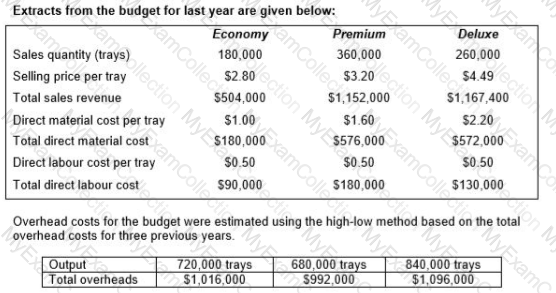

Question # 11

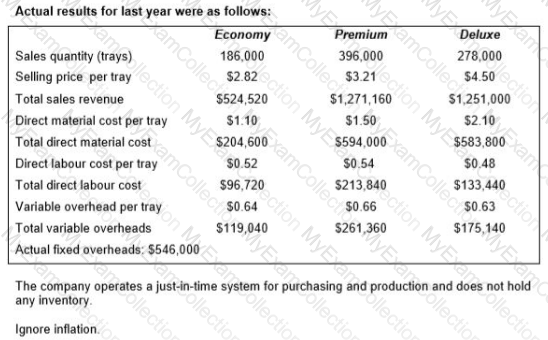

A company produces trays of pre-prepared meals that are sold to restaurants and food retailers. Three varieties of meals are sold: economy, premium and deluxe.

Calculate, for the original budget, the budgeted fixed overhead costs, the budgeted variable overhead cost per tray and the budgeted total overheads costs.

Question # 12

Explain the advantages of management participation in budget setting and the potential problems that may arise in the use of the resulting budget as a control mechanism.

Select all the correct answers.

Question # 13

A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company’s planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company’s normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning.

The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

Select ALL the benefits for the company that could occur following the introduction of an activity based budgeting system.

Question # 14

Which of the following explain why standard costing is less appropriate in the contemporary business environment?

1. In a continuous improvement environment standard costing can restrict the impetus to remain as cost competitive as rivals.

2. Fixed overhead variances are less relevant as fixed costs represent a decreasing proportion of total manufacturing cost.

3. In a just-in-time environment there are fewer costs to control.

Question # 16

Some of the movements in a time series follow a pattern over time.

Which type of movement does NOT follow a pattern over time?

Question # 17

Your company want to know how many units they'd have to sell this season to break even. However, you have some reservations over whether or not breakeven analysis is suitable for the company.

Which of these assumptions over product range limit the accuracy of break even analysis? Select ALL that apply.

Question # 18

A company's initial budget for month 3 includes sales of $100,000, a contribution to sales (C/S) ratio of 40% and fixed costs of $20,000.

If the budgeted sales volume in month 3 is reduced by 5% but contribution per unit, total fixed costs and sales mix are unchanged, which of the following statements, about the change to the budgeted profit or contribution in month 3 is true?

Question # 19

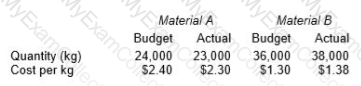

A company produces a product that requires two materials, Material A and Material B. Details of the material quantities and costs for August are given in the table below.

Budgeted and actual output of the product for August was 12,000 units.

The material yield variance for August is:

Question # 20

A company is considering the use of Material V in a special order.

The material is used regularly and a sufficient quantity of the material is in inventory.

It could also be sold, at just below the current market price, to a local competitor.

What is the relevant cost of Material V to be used in the special contract?

Question # 21

A manufacturing company produces and sells a single product.

It is preparing its budget for the next period and expects to breakeven.

Budgeted fixed costs are the same as budgeted variable costs and the budgeted contribution to sales ratio is 50%.

If all budgeted costs decreased by 10%, which of the following statements is true?

Question # 22

8fb9be1c-b0d5-4acb-8cfb-f4b4426e641B. The primary objective of Company A is to maximise profit. It is now deciding on the optimum production mix for the next period and has one limited production resource.

The production mix decision should be based on:

Question # 23

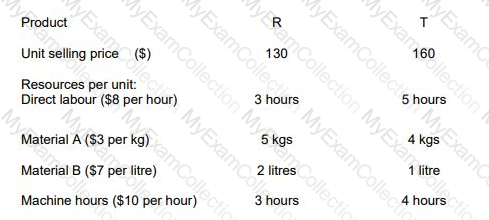

RT produces two products from different quantities of the same resources using a just-in-time (JIT) production system. The selling price and resource requirements of each of the products are shown below:Â

Market research shows that the maximum demand for products R and T during June 2010 is 500 units and 800 units respectively. This does not include an order that RT has agreed with a commercial customer for the supply of 250 units of R and 350 units of T at selling prices of $100 and $135 per unit respectively. Although the customer will accept part of the order, failure by RT to deliver the order in full by the end of June will cause RT to incur a $10,000 financial penalty. At a recent meeting of the purchasing and production managers to discuss the production plans of RT for June, the following resource restrictions for June were identified: Direct labour hours 7,500 hours

Material A 8,500 kgs

Material B 3,000 litres

Machine hours 7,500 hours

(Refer to previous 2 questions.)

You have now presented your optimum production plan to the purchasing and production managers of RT. During your presentation it became clear that the predicted resource restrictions were rather optimistic. In fact, the managers agreed that the availability of all of the resources could be as much as 10% lower than their original predictions.

Assuming that RT completes the order with the commercial customer, and using linear programming, show the optimum production plan for RT for June 2010 on the basis that the availability of all resources is 10% lower than originally predicted.Â

Question # 25

Sales volumes reported for the latest period are used by managers as the basis to forecast sales for the forthcoming period. The forecasts are compared with the budgeted sales and plans are adjusted to ensure that the budgeted sales are achieved.

This is an example of:

Question # 26

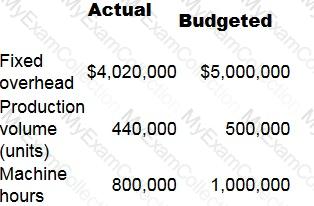

Company Y absorbs fixed production overheads using a rate per machine hour. Budgeted and actual data for month 8 are as follows:

What is the fixed production overhead efficiency variance?

Question # 27

How would the cost of recycling scrap be classified in an environmental costing system?

Question # 28

Which of the following statements about total quality management are incorrect? Select ALL that apply.

Question # 29

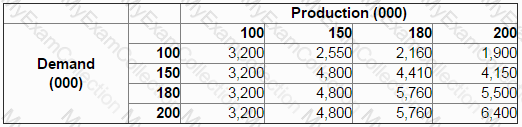

A company is launching a new product.

The company accountant has constructed a payoff table to show the estimated profit at different levels of production and demand.

How many units should the company produce if the minimax regret criterion is applied?

Question # 30

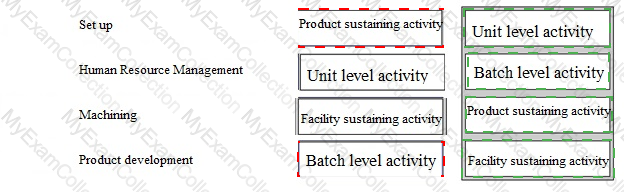

Place each activity against the correct category according to its classification in the cost hierarchy of activities.

Question # 31

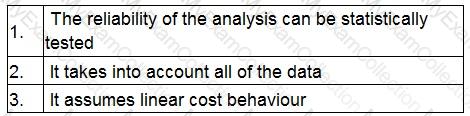

The following statements relate to the advantage(s) that linear regression has over the high-low method in the analysis of cost behaviour:

Which statement(s) is/are true?

Question # 32

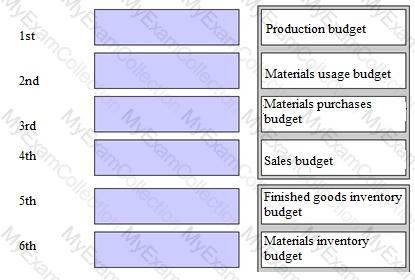

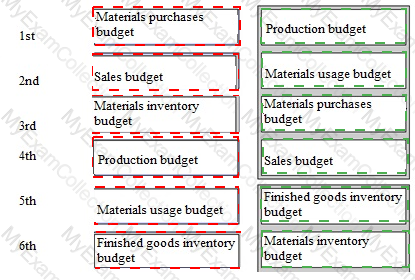

For a company that does not have any production resource limitations, what would be the correct sequence for budget preparation?

Question # 33

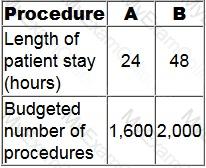

A clinic offers two types of procedure, A and B.

The clinic uses activity-based costing. The general facility overhead cost for next year is budgeted to be $8,601,600. The cost driver is the length of patient stay.

Additional data:

What is the general facility overhead cost for each Procedure B?

Question # 34

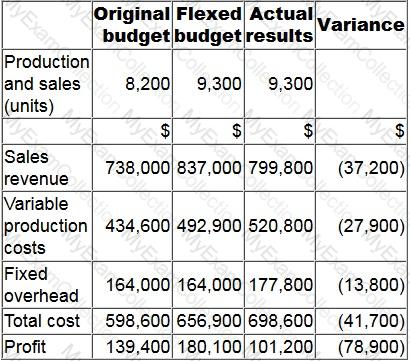

The budgetary control report of XYZ for the latest period is shown below. Variances in brackets are adverse.

What is the sales volume profit variance?

Question # 35

Select the benefits to a company of using sensitivity analysis in investment appraisal.

(Select all the true statements.)

Question # 36

When a moving average is plotted onto a graph, where should the plotted points be located?

Question # 37

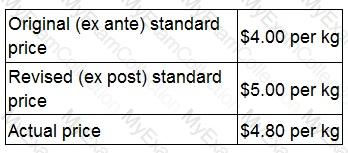

A company reports planning and operational variances to its managers. The following data are available concerning the price of direct material M in the last period. Material M is the only material used by the company. The company operates a just-in-time (JIT) purchasing system.

Which TWO of the following statements about last period are definitely correct based on this information?

The direct material price operational variance was adverse.

Question # 38

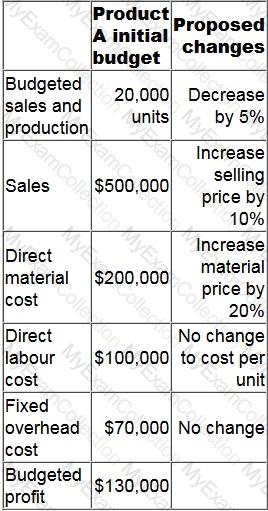

Company M is preparing its budgeted profit statement for the next year.

The initial budget for Product A is as follows with some changes proposed by the sales director to increase the quality of the product.

What would the budgeted profit of Product A be if the proposed changes are made?

Give your answer as a whole number.

Question # 39

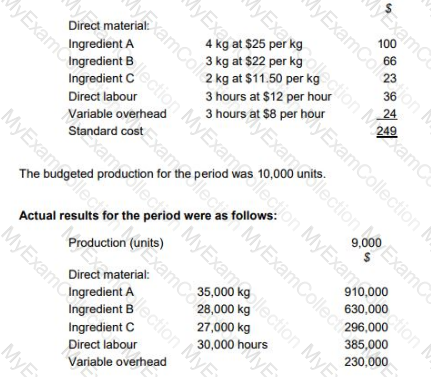

TP makes wedding cakes that are sold to specialist retail outlets which decorate the cakes according to the customers’ specific requirements. The standard cost per unit of its most popular cake is as follows:

The general market prices at the time of purchase for Ingredient A and Ingredient B were $23 per kg and $20 per kg respectively.

TP operates a JIT purchasing system for ingredients and a JIT production system; therefore, there was no inventory during the period.

Prepare a statement which reconciles the flexed budget material cost and the actual material cost. Your statement should include the material price planning variances, and the operational variances including material price, material mix and material yield.

What was the material price planning variance for ingredient A?