Question # 4

Which of the following disbursement techniques can be used to ensure timely payments?

A.

warrants

B.

checks

C.

drafts

D.

bank cards

Full Access

Answer:

C

Explanation:

ï‚· What Are Disbursement Techniques?

Disbursement techniques refer to the methods used by organizations to pay vendors or settle financial obligations. The timeliness of payments depends on the technique used.

ï‚· Why Are Drafts the Best Option for Timely Payments?

Adraftis a payment instrument issued by an organization’s bank, drawn against its account, and typically includes specific payment timing instructions.

Drafts allow the payer to specify the timing of payments, ensuring they are made on time.

ï‚· Why Other Options Are Incorrect:

A. Warrants:Warrants authorize payments but do not ensure timeliness as they require additional processing before funds are disbursed.

B. Checks:Checks rely on postal delivery and clearing times, which may delay payments.

D. Bank cards:While convenient, bank cards are typically used for immediate payments, not for ensuring future timely disbursements.

ï‚· References and Documents:

Treasury Financial Manual:Highlights drafts as a disbursement tool for controlling the timing of payments.

GAO Cash Management Guide:Discusses the benefits of drafts in ensuring timely payments.

Question # 5

A key element in coputer-assisted audit techniques is

A.

writing the system audit program.

B.

verifying internal controls.

C.

obtaining appropriate data.

D.

purchasing data mining software.

Full Access

Answer:

C

Explanation:

Definition of Computer-Assisted Audit Techniques (CAATs):

CAATs use software tools to perform audit tasks such as data analysis, testing transactions, and evaluating internal controls.

Obtaining accurate and relevant data is a key first step, as it forms the basis of any analysis performed using CAATs.

Explanation of Answer Choices:

A. Writing the system audit program: This is part of audit planning but not a specific feature of CAATs.

B. Verifying internal controls: While CAATs can be used to test controls, obtaining data is fundamental to this process.

C. Obtaining appropriate data: Correct. CAATs rely on accurate, relevant, and complete data for meaningful analysis.

D. Purchasing data mining software: While software is a tool for CAATs, the focus is on using data, not on acquiring the software itself.

[:, Information Systems Audit and Control Association (ISACA),Guide to Computer-Assisted Audit Techniques., Association of Government Accountants (AGA),Data Analytics and Auditing Best Practices., ]

Question # 6

A key objective of a performance audit is

A.

providing an opinion on the entity's financial statement.

B.

assessing program effectiveness, economy and efficiency.

C.

providing an opinion on a subject matter that is the responsibility of another party.

D.

issuing a report of findings based upon an agreed-upon procedure.

Full Access

Answer:

B

Explanation:

Performance Audit Objectives:

Performance audits evaluate theeffectiveness,efficiency, andeconomyof government programs, operations, or activities.

These audits focus on improving operations, achieving program goals, and ensuring responsible use of public resources.

Explanation of Answer Choices:

A. Providing an opinion on the entity's financial statement: This is the objective of a financial statement audit, not a performance audit.

B. Assessing program effectiveness, economy, and efficiency: Correct. This is the primary objective of performance audits.

C. Providing an opinion on a subject matter that is the responsibility of another party: This aligns with attestation engagements, not performance audits.

D. Issuing a report of findings based upon an agreed-upon procedure: This describes agreed-upon procedures engagements, not performance audits.

[:, GAO,Government Auditing Standards (Yellow Book)., Association of Government Accountants (AGA),Performance Auditing Guidance., ]

Question # 7

Federal entities primarily assess internal controls to

A.

confirm that all management objectives will be met.

B.

identify program areas where efficiencies may be gained.

C.

ensure there is no fraud, waste or abuse within the entity.

D.

determine what legislation is not applicable to the entity.

Full Access

Answer:

B

Explanation:

Federal Entities and Internal Controls:

Federal entities assess internal controls to ensure efficient, effective, and economical use of resources while achieving program objectives.

Internal control assessments often identify areas for improvement, such as reducing waste or increasing operational efficiency.

Explanation of Answer Choices:

A. Confirm that all management objectives will be met: Internal controls reduce risk but do not guarantee all objectives will be achieved.

B. Identify program areas where efficiencies may be gained: Correct. Internal controls are assessed to optimize operations and identify improvements.

C. Ensure there is no fraud, waste, or abuse within the entity: While controls mitigate risks of fraud, waste, or abuse, assessments aim to identify opportunities for efficiency.

D. Determine what legislation is not applicable to the entity: This is unrelated to internal control assessments.

[:, GAO,Standards for Internal Control in the Federal Government (Green Book)., Office of Management and Budget (OMB),Circular A-123, Internal Control Systems., ]

Question # 8

An agency benefit program allows employees who commute by public transit up to 10 free taxi trips home per

calendar year. Employees can use the program for personal or family health emergencies. The most appropriate

method to check for abuse of this program is

A.

using program data to look for instances of individuals using the service more than 10 times per year.

B.

using geographic information system data to determine if the destination addresses were hospitals or

clinics.

C.

using personal data to determine if the destination address matches the employees home address.

D.

requesting records from a random sample of employees to verify they used transit on the day they

used the taxi services.

Full Access

Answer:

D

Explanation:

ï‚· Why Verify Transit Use Before Taxi Use?

The program is intended for employees who commute by public transit. Verifying transit use on the day the taxi service was used ensures employees are adhering to program rules.

Random sampling is cost-effective and practical for identifying abuse without needing to review all records.

ï‚· Why Other Options Are Incorrect:

A. Looking for individuals using the service more than 10 times:This only identifies overuse but does not confirm whether program rules were followed.

B. Checking destination addresses for hospitals/clinics:This assumes all emergencies involve medical visits, which is not always the case.

C. Matching destination addresses to home addresses:This does not confirm transit use and may not identify abuse of the program.

ï‚· References and Documents:

GAO Fraud Prevention Guide:Recommends using random sampling to check compliance with program rules.

Best Practices for Internal Controls in Benefit Programs:Emphasizes verifying eligibility and usage to detect potential abuse.

Question # 9

A program manager at a local agency needs to understand if program participation varies significantly from enrollment. The information changes daily. The best way to quickly analyze this would be to use

A.

crosstab.

B.

portable document format.

C.

text file.

D.

dashboard.

Full Access

Answer:

D

Explanation:

Analyzing Participation and Enrollment Trends:

Dashboards are tools that provide real-time visualizations of data, making them ideal for quickly analyzing trends such as program participation versus enrollment.

They allow program managers to view up-to-date metrics and identify variances without manual data processing.

Explanation of Answer Choices:

A. Crosstab: While useful for comparing categorical data, crosstabs are static and less effective for real-time analysis.

B. Portable document format (PDF): A PDF is a static file format, unsuitable for dynamic data analysis.

C. Text file: Text files provide raw data but require additional processing, making them inefficient for quick analysis.

D. Dashboard: Correct. Dashboards provide dynamic, real-time analytics, perfect for monitoring daily changes in participation and enrollment.

[:, Association of Government Accountants (AGA),Data Visualization in Public Sector Management., Government Performance Lab,Using Dashboards for Real-Time Program Management., ]

Question # 10

What type of analygis should a finance director use to determine if there will be enough funds available to cover bills

due within the next 30 days?

A.

quick/current ratio

B.

receivables turnover ratio

C.

budgetary cushion ratio

D.

debt burden ratio

Full Access

Answer:

A

Explanation:

Purpose of the Analysis:A finance director needs to assess whether the organization has enough funds available to cover short-term obligations (bills due within 30 days). This requires evaluating liquidity.

Explanation of Key Ratios:

Quick/Current Ratio: Measures an entity’s ability to pay its short-term liabilities using liquid assets.

Current Ratio= Current Assets ÷ Current Liabilities.

Quick Ratioexcludes less liquid assets (e.g., inventory), focusing on assets that can quickly convert to cash.This is the appropriate measure for assessing immediate liquidity.

Receivables Turnover Ratio: Measures how efficiently receivables are collected but doesn’t directly evaluate liquidity for bills due within 30 days.

Budgetary Cushion Ratio: Refers to financial reserves relative to annual spending, not short-term liquidity.

Debt Burden Ratio: Evaluates debt relative to revenues but does not address immediate cash flow needs.

[:, Government Finance Officers Association (GFOA),Liquidity Management Best Practices., Association of Government Accountants (AGA),Financial Statement Analysis for Government Finance Officers., ]

Question # 11

According to OMB Circular A-50, who holds personal responsibility for ensuring that disagreements with audit

findings and recommendations are resolved?

A.

comptroller general

B.

OMB deputy director for management

C.

inspector general

D.

audit follow-up official

Full Access

Answer:

D

Explanation:

ï‚· What Does OMB Circular A-50 Require?

OMB Circular A-50establishes policies for resolving and following up on audit findings and recommendations. It assignspersonal responsibilityto anaudit follow-up officialwithin the agency for ensuring that disagreements with audit findings are resolved and that corrective actions are implemented.

ï‚· Why Is the Audit Follow-Up Official Responsible?

The follow-up official ensures the agency responds appropriately to audit findings, tracks corrective actions, and resolves disagreements in a timely manner. This ensures accountability and compliance with audit recommendations.

ï‚· Why Other Options Are Incorrect:

A. Comptroller General:The Comptroller General leads the GAO and oversees audits but is not responsible for resolving disagreements within agencies.

B. OMB Deputy Director for Management:Provides guidance on audit policies but does not hold personal responsibility for resolving disagreements.

C. Inspector General:Performs audits and investigations but does not resolve disagreements over audit findings.

ï‚· References and Documents:

OMB Circular A-50:Specifies that the audit follow-up official holds responsibility for resolving disagreements.

GAO Yellow Book:Discusses the roles and responsibilities of various officials in audit processes.

Question # 12

A single audit report will include an opinion or disclaimer of opinion that the financial statements are

A.

free from fraud.

B.

fairly presented in accordance with GAAP.

C.

fairly presented in accordance with GASB.

D.

fairly presented in accordance with GAO.

Full Access

Answer:

B

Explanation:

Single Audit Report Requirements:

A single audit evaluates the financial statements and compliance with federal award requirements.

Thefinancial statement opinionmust state whether the financial statements arefairly presented in accordance with Generally Accepted Accounting Principles (GAAP).

Explanation of Answer Choices:

A. Free from fraud: Incorrect. Auditors do not provide an opinion on fraud; they assess for material misstatements.

B. Fairly presented in accordance with GAAP: Correct. The financial statement opinion is issued based on compliance with GAAP.

C. Fairly presented in accordance with GASB: Incorrect. GASB (Governmental Accounting Standards Board) provides guidance for state and local governments, but financial statements must comply with GAAP as the overarching standard.

D. Fairly presented in accordance with GAO: Incorrect. The GAO (Government Accountability Office) issues auditing standards, not financial reporting standards.

[:, OMB Uniform Guidance (2 CFR Part 200),Subpart F - Audit Requirements., GAO,Government Auditing Standards (Yellow Book)., ]

Question # 13

All of the following ae among the stated purposes of GPRA EXCEPT to

A.

help managers improve service delivery.

B.

improve internal management practices.

C.

provide instructions on program reporting.

D.

improve program effectiveness.

Full Access

Answer:

C

Explanation:

ï‚· What Is GPRA?

TheGovernment Performance and Results Act (GPRA)of 1993 was designed to improve the performance of federal programs by requiring federal agencies to establish goals, measure performance, and report on their progress.

ï‚· Stated Purposes of GPRA:

Improve Service Delivery (Option A):GPRA helps agencies align performance goals with customer needs, improving service delivery.

Improve Internal Management Practices (Option B):By requiring performance metrics and evaluations, GPRA enhances internal management and decision-making processes.

Improve Program Effectiveness (Option D):GPRA aims to make federal programs more effective by fostering accountability and linking resources to results.

ï‚· Why Option C Is Incorrect:

GPRA does not provide detailedinstructions on program reporting.While it requires agencies to report on their performance, it does not dictate the specific steps or instructions for reporting. Instead, agencies design their own reporting processes within the GPRA framework.

ï‚· References and Documents:

Government Performance and Results Act of 1993:Stipulates the law’s objectives but does not mention program reporting instructions.

GAO Report on GPRA Implementation:Highlights GPRA’s purpose to improve performance management and accountability without prescribing reporting instructions.

Question # 14

In an internal control evaluation, what are the roles of management and the auditor regarding the risk of fraud, waste and abuse?

A.

Management identifies risks, auditors assess control effectiveness.

B.

Auditors identify risks, management implements control measures.

C.

Both management and auditors determine risk tolerance levels.

D.

Management mitigates risks, auditors monitor compliance with controls.

Full Access

Answer:

A

Explanation:

ï‚· Role of Management in Internal Control Evaluation:

Responsibility for Risk Identification:Management has the primary responsibility for designing, implementing, and maintaining an effective system of internal controls. As part of this process, management identifies the risks related to fraud, waste, and abuse that could impact financial reporting or operational efficiency.

Mitigating Risks:Once risks are identified, management is responsible for mitigating them by developing appropriate policies, procedures, and controls.

ï‚· Role of the Auditor in Internal Control Evaluation:

Assessing Control Effectiveness:Auditors are not responsible for designing or implementing controls; rather, their role is to evaluate whether the controls put in place by management are effective. They do this through testing, observation, and other audit procedures.

Fraud Risk Assessment:As part of their duties under Generally Accepted Government Auditing Standards (GAGAS), auditors must assess the risk of material misstatement due to fraud and evaluate how management’s controls address those risks.

ï‚· Why Other Options Are Incorrect:

B.Auditors do not identify risks—this is management's job. Auditors evaluate and assess the controls already in place.

C.Determining risk tolerance is a governance and management responsibility, not the joint responsibility of auditors and management.

D.Management mitigates risks, but auditors don’t monitor compliance with controls—they test and evaluate the controls as part of their audit procedures.

ï‚· References and Documents:

GAGAS (Yellow Book) by GAO:Emphasizes management’s responsibility for risk identification and the auditor’s responsibility for assessing control effectiveness.

COSO Internal Control Framework (2013):Highlights management’s responsibility for risk assessment and control design, while auditors provide independent assurance.

Question # 15

Earned value management is preferred over traditional project management because

A.

earned value management is used to monitor progress and deliverables of smaller projects.

B.

earned value management provides information about status of deliverables, funds and time expended.

C.

traditional project management is used to monitor progress and deliverables of larger projects.

D.

traditional project management provides information about status of deliverables, funds and time expended.

Full Access

Answer:

B

Explanation:

ï‚· What Is Earned Value Management (EVM)?

EVMis a project management methodology that integrates scope, cost, and schedule to measure project performance. It provides a comprehensive view of progress by combining information about deliverables (work completed), funds (budget spent), and time (schedule adherence).

ï‚· Why Is EVM Preferred Over Traditional Project Management?

EVM offers a holistic view of project performance by quantifying progress and comparing it to planned performance, allowing for proactive decision-making.

Traditional project management often focuses on individual aspects (e.g., timelines or budgets) without integrating them as effectively as EVM.

ï‚· Why Other Options Are Incorrect:

A. EVM monitors smaller projects:EVM is not restricted to small projects; it is widely used for complex, large-scale projects.

C. Traditional project management is used for larger projects:This is incorrect—both methodologies can be used for projects of any size.

D. Traditional project management provides status on deliverables, funds, and time:This is inaccurate; traditional methods often lack the integrated performance tracking provided by EVM.

ï‚· References and Documents:

GAO Guide to Project Management:Recommends EVM for comprehensive performance tracking.

PMBOK (Project Management Body of Knowledge):Details the advantages of EVM over traditional project management.

Question # 16

Government performance measurement promotes

A.

responsibility.

B.

profitability.

C.

accountability.

D.

cash availability.

Full Access

Answer:

C

Explanation:

ï‚· What Is Government Performance Measurement?

Government performance measurement is the process of setting goals, tracking progress, and evaluating outcomes for government programs and services. This system ensures that public funds are used effectively and that programs achieve intended results.

ï‚· How Does It Promote Accountability?

Accountability is the primary goal of performance measurement. It holds government officials and agencies responsible for managing public resources efficiently and achieving measurable outcomes.

By measuring performance, governments can transparently demonstrate how resources are being used and whether programs are meeting their objectives.

ï‚· Why Other Options Are Incorrect:

A. Responsibility:While responsibility is important, it refers more to the assignment of duties, not the system of holding entities accountable.

B. Profitability:Governments are not profit-driven organizations; their focus is on service delivery, not profits.

D. Cash Availability:Performance measurement focuses on outcomes, not managing cash flows.

ï‚· References and Documents:

Government Performance and Results Act (GPRA):Promotes accountability through performance measurement and reporting.

GAO Report on Performance Accountability:Emphasizes the role of performance measurement in achieving government accountability.

Question # 17

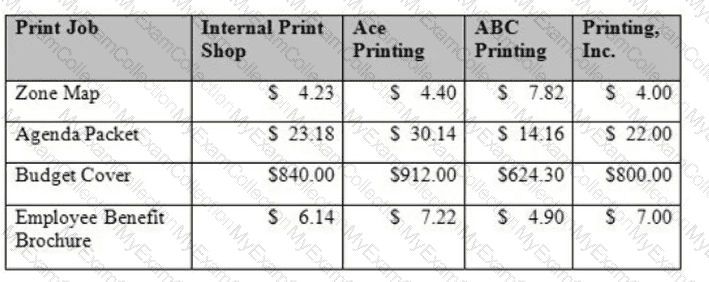

Based on the data below, what can be concluded about outsourcing print job?

A.

It is better to keep the printing in-house.

B.

Outsourcing printing is feasible.

C.

Outsourcing printing is necessary.

D.

ABC Printing should be awarded the outsourcing contract.

Full Access

Answer:

B

Explanation:

Understanding the Scenario:The table compares the costs of four printing jobs performed by an "Internal Print Shop" versus three external vendors (Ace Printing, ABC Printing, and Printing, Inc.). Each vendor's pricing varies by print job type. The task is to evaluate whether outsourcing (hiring external vendors) is a reasonable alternative to keeping the work in-house.

Key Considerations in Outsourcing:According to governmental accounting principles and budgeting practices outlined by theAssociation of Government Accountants (AGA), the decision to outsource should consider:

Cost-effectiveness: Does outsourcing reduce costs without compromising quality or service delivery?

Operational efficiency: Can outsourcing free up internal resources for other priorities?

Comparative pricing: How do external vendor rates compare to internal costs for identical services?

Analysis of the Print Jobs:Let’s break down the cost comparison for each print job:

Zone Map:Internal cost = $4.23.Cheapest vendor = Printing, Inc., at $4.00.Outsourcing is cheaper for this job.

Agenda Packet:Internal cost = $23.18.Cheapest vendor = Printing, Inc., at $22.00.Outsourcing is cheaper for this job.

Budget Cover:Internal cost = $840.00.Cheapest vendor = ABC Printing, at $624.30.Outsourcing is significantly cheaper for this job.

Employee Benefit Brochure:Internal cost = $6.14.Cheapest vendor = ABC Printing, at $4.90.Outsourcing is cheaper for this job.

Conclusion Based on Analysis:

Across all four print jobs, the lowest-cost external vendor always beats the Internal Print Shop's costs.

From abudgetary perspective, outsourcing is feasible as it offers cost savings across all jobs.

Why Not A, C, or D?:

Option A(Keep printing in-house): Incorrect, as in-house costs are consistently higher than the cheapest external vendor.

Option C(Outsourcing is necessary): Incorrect, as feasibility doesn’t mean necessity; internal printing is still an option if other factors (like quality or control) outweigh costs.

Option D(Award contract to ABC Printing): Incorrect, since the best vendor depends on the job (e.g., Printing, Inc. is cheaper for Zone Map and Agenda Packet).

[:, Association of Government Accountants (AGA),Government Financial Manager Certification Study Guide: Budgeting, Cost Accounting, and Auditing Principles., Government Finance Officers Association (GFOA),Best Practices in Outsourcing and Procurement., Federal Accounting Standards Advisory Board (FASAB),Cost Accounting Standards for Governmental Operations., , ]

Question # 18

Which element of an inventory management system includes determining how much stock to have on hand?

A.

inventory control

B.

safeguard control

C.

management control

D.

supply control

Full Access

Answer:

A

Explanation:

ï‚· What Is Inventory Control?

Inventory controlrefers to the processes and systems used to manage stock levels, including determining how much inventory to keep on hand, reordering stock, and maintaining optimal levels to meet operational needs while minimizing costs.

Determining stock levels is a central function of inventory control, ensuring the organization has the right amount of inventory to meet demand without overstocking or understocking.

ï‚· Why Other Options Are Incorrect:

B. Safeguard control:This refers to protecting inventory from theft, damage, or loss, not determining stock levels.

C. Management control:This is a broader term encompassing oversight and governance, not specific to inventory.

D. Supply control:This typically refers to managing supply chains and suppliers, not the internal control of inventory levels.

ï‚· References and Documents:

GAO Inventory Management Guide:Defines inventory control as the process of determining and maintaining appropriate stock levels.

Best Practices in Government Inventory Management (AGA):Emphasizes the role of inventory control in balancing supply and demand.

Question # 19

One of the five components of COSO ERM is

A.

performance.

B.

changing environment.

C.

complex calculations.

D.

accepting risk.

Full Access

Answer:

A

Explanation:

ï‚· What Is COSO ERM?

TheCOSO Enterprise Risk Management (ERM) Frameworkis a widely accepted framework that helps organizations identify, assess, and manage risks while creating value. The five components of COSO ERM are:

Governance and Culture

Strategy and Objective-Setting

Performance

Review and Revision

Information, Communication, and Reporting

ï‚· Why Is Performance a Key Component?

ThePerformancecomponent focuses on identifying, assessing, and prioritizing risks to achieving an organization’s objectives. It includes implementing risk responses (e.g., avoiding, reducing, sharing, or accepting risks) and monitoring their effectiveness.

ï‚· Why Other Options Are Incorrect:

B. Changing Environment:This is not a COSO ERM component but a general factor influencing risk management.

C. Complex Calculations:This is not relevant to COSO ERM.

D. Accepting Risk:While accepting risk is part of risk responses, it is not one of the five COSO ERM components.

ï‚· References and Documents:

COSO ERM Framework (2017):Details the five components of ERM and their application in managing risks.

Question # 20

Using Benford Digital Analysis, an auditor can identify potential fraud when

A.

a higher-than-expected number of payment amounts to one vendor start with the number three.

B.

a large number of contracts are awarded to one vendor.

C.

a large contract is awarded to the director's close relative.

D.

an employee receives kickbacks from real estate developers.

Full Access

Answer:

A

Explanation:

Benford's Law and Fraud Detection:

Benford's Lawis a statistical principle that predicts the frequency of leading digits in naturally occurring datasets.

Deviations from the expected distribution (e.g., a higher-than-expected frequency of a specific leading digit) can indicate manipulation or fraud.

For example, if too many payments start with the number "3," it suggests potential tampering.

Explanation of Answer Choices:

A. A higher-than-expected number of payment amounts to one vendor start with the number three: Correct. This aligns with how Benford’s Law is used to detect anomalies in numerical data.

B. A large number of contracts are awarded to one vendor: While concerning, this is not related to Benford’s Law.

C. A large contract is awarded to the director's close relative: This indicates a conflict of interest but is unrelated to Benford’s Law.

D. An employee receives kickbacks from real estate developers: This is fraud but cannot be identified using Benford’s Law.

[:, Association of Certified Fraud Examiners (ACFE),Fraud Detection Using Benford’s Law., GAO,Fraud Risk Management Framework., ]

Question # 21

What might be a cost-effective solution for a local public school to reduce increasing special education costs without violating federal maintenance of effort requirements?

A.

Shift a portion of the costs in the form of a fee to parents.

B.

Decrease budget allocation for special education services.

C.

Develop a shared services agreement with surrounding districts.

D.

Outsource special needs services to a private contractor.

Full Access

Answer:

C

Explanation:

ï‚· Why Shared Services Agreements Are Cost-Effective:

A shared services agreement allows multiple school districts to pool resources and share the costs of special education services, such as specialized staff, transportation, or facilities.

This reduces duplication of services, increases efficiency, and helps lower costs without reducing the quality of education provided.

ï‚· Why Federal Maintenance of Effort (MOE) Requirements Matter:

Under federal law, schools must maintain a certain level of funding for special education services to receive federal grants. Cutting budgets or shifting costs directly to parents would likely violate MOE requirements.

ï‚· Why Other Options Are Incorrect:

A. Shift a portion of the costs in the form of a fee to parents:This violates federal regulations, as public schools cannot charge parents for special education services.

B. Decrease budget allocation for special education services:This would also violate MOE requirements and reduce services for students with special needs.

D. Outsource special needs services to a private contractor:While outsourcing can be an option, it may not always reduce costs and could introduce additional risks (e.g., quality concerns or compliance issues).

ï‚· References and Documents:

Individuals with Disabilities Education Act (IDEA):Mandates federal MOE requirements for special education funding.

GAO Report on Shared Services in Education:Highlights cost-saving benefits of shared services agreements.

Question # 22

According to OMB Circular A-11, what analytical method should be used to measure the cost, schedule and performance goals of a capital asset acquisition project?

A.

earned value management

B.

net present value

C.

future value

D.

regression analysis

Full Access

Answer:

A

Explanation:

OMB Circular A-11 and Capital Asset Acquisition:

OMB Circular A-11 mandates the use ofearned value management (EVM)for measuring cost, schedule, and performance goals in capital asset acquisition projects.

EVM integrates project scope, schedule, and cost data to assess project performance and forecast outcomes.

Explanation of Answer Choices:

A. Earned value management: Correct. EVM is the prescribed method for tracking progress on capital projects under OMB Circular A-11.

B. Net present value: Used for financial analysis, such as determining the economic value of future cash flows, but not for tracking project progress.

C. Future value: Measures the value of an investment at a future point, not applicable to project tracking.

D. Regression analysis: A statistical method for identifying relationships between variables, not for measuring project performance.

[:, OMB Circular A-11,Capital Programming Guide., U.S. General Services Administration (GSA),Earned Value Management Implementation., ]

Question # 23

A sound investment category for pension funds that can be easily valued is

A.

open-ended mutual funds.

B.

reverse repurchase agreements.

C.

derivative instruments.

D.

internal investment pools.

Full Access

Answer:

A

Explanation:

ï‚· What Are Open-Ended Mutual Funds?

Open-ended mutual funds are investment vehicles that allow investors to buy and sell shares at the current net asset value (NAV), which is determined daily.

These funds are highly liquid and can be easily valued, making them a sound investment option for pension funds.

ï‚· Why Are They Suitable for Pension Funds?

Pension funds require investments that are easily valued, transparent, and provide liquidity to meet benefit obligations. Open-ended mutual funds meet all these criteria.

ï‚· Why Other Options Are Incorrect:

B. Reverse repurchase agreements:While they can be part of investment strategies, they are not easily valued compared to open-ended mutual funds.

C. Derivative instruments:Derivatives can be complex and difficult to value, making them less suitable for pension funds that prioritize transparency and simplicity.

D. Internal investment pools:These are investment vehicles used by governments, but their valuation may not be as straightforward or frequent as mutual funds.

ï‚· References and Documents:

GAO Guide to Investment Management for Pension Funds:Recommends transparent, easily valued investments like mutual funds.

AICPA Pension Plan Audit Guidelines:Emphasizes liquidity and valuation in pension fund investments.

Question # 24

An evaluation of anggntity’s single year financial statements would use which of the following analyses?

A.

comparative

B.

horizontal

C.

trend

D.

vertical

Full Access

Answer:

D

Explanation:

ï‚· What Is Vertical Analysis?

Vertical Analysisevaluates a single year's financial statements by expressing each line item as a percentage of a base amount. For example, in an income statement, each expense may be presented as a percentage of total revenue.

This approach helps users understand the relative size of each financial statement item within the context of the total.

ï‚· Why Is Vertical Analysis Used for a Single Year?

Vertical analysis focuses solely on relationships within a single set of financial statements, making it the appropriate choice for single-year evaluations.

ï‚· Why Other Options Are Incorrect:

A. Comparative:Involves comparing financial data across entities or periods, not within a single year.

B. Horizontal:Focuses on changes in financial data over time (year-to-year comparisons).

C. Trend:Examines patterns over multiple periods to identify long-term trends, not a single year.

ï‚· References and Documents:

GAO Financial Audit Manual:Recommends vertical analysis for single-year financial statement evaluations.

AICPA Financial Statement Analysis Guide:Provides detailed examples of vertical analysis techniques.

Question # 25

The Federal Credit Reform Act requires complex calculations, which are likely to include errors. This is an example of

A.

audit risk.

B.

control risk.

C.

detection risk.

D.

inherent risk.

Full Access

Answer:

D

Explanation:

ï‚· Definition of Inherent Risk:

Inherent risk refers to the risk of material misstatement in financial statements or other reports due to the nature of the subject matter, without considering any controls in place. It arises from the complexity, judgment, or uncertainty involved in the underlying transactions or calculations.

ï‚· Why This Is Inherent Risk:

TheFederal Credit Reform Actrequires complex calculations to estimate loan subsidies, interest rates, and cash flows. These calculations inherently involve significant judgment and estimation, making them prone to errors. This is a classic example of inherent risk because the complexity exists regardless of controls.

ï‚· Why Other Options Are Incorrect:

A. Audit Risk:This refers to the overall risk that the auditor may issue an incorrect opinion. In this case, the issue is about the inherent complexity of the calculations, not the auditor’s procedures.

B. Control Risk:This is the risk that errors will not be prevented or detected due to weak internal controls. While control risk could contribute to misstatements, it is not the primary issue in this example.

C. Detection Risk:This is the risk that auditors will not detect a misstatement. This risk relates to audit procedures, not the inherent complexity of the calculations.

ï‚· References and Documents:

GAO Yellow Book on Risk Assessment:Explains inherent risk in the context of government financial reporting.

AICPA Standards on Audit Risk (AU-C 315):Highlights inherent risk as arising from the nature of transactions or subject matter.

Question # 26

What is the most fupdamental cash control?

A.

segregation of duties

B.

use of automated systems

C.

analysis of cash reports

D.

frequent reconciliation of bank accounts

Full Access

Answer:

D

Explanation:

Cash Control Fundamentals:

The primary goal of cash controls is to safeguard assets and prevent fraud, errors, or misappropriation.

Frequent bank reconciliations ensure that recorded cash balances match actual bank balances, detecting discrepancies quickly.

Explanation of Answer Choices:

A. Segregation of duties: While critical for cash management, it is not the most fundamental cash control.

B. Use of automated systems: Helpful for efficiency but not a fundamental control.

C. Analysis of cash reports: Important, but reconciling bank accounts is more critical for detecting errors or fraud.

D. Frequent reconciliation of bank accounts: Correct. This is the most fundamental and widely recognized control for safeguarding cash.

[:, Association of Government Accountants (AGA),Cash Management Best Practices., Government Finance Officers Association (GFOA),Bank Reconciliation Best Practices., ]

Question # 27

A capital asset transferred to another department within the same government should be

A.

recorded with the original department to maximize receipts.

B.

recorded with the second department to minimize costs.

C.

retained in the government's fixed asset tracking system with no change in book value to either department.

D.

retained in the government's fixed asset tracking system showing the book value of the asset transferred to the receiving department.

Full Access

Answer:

D

Explanation:

ï‚· Capital Asset Transfers Within the Same Government:

When a capital asset is transferred between departments within the same government, the asset’sbook value(its original cost minus accumulated depreciation) should remain in the fixed asset tracking system.

The transfer does not change the overall value of the asset for the government as a whole, but it should reflect that the asset is now under the responsibility of the receiving department.

ï‚· Why This Is Important:

Accurate tracking ensures the fixed asset system reflects the current custodian of the asset and allows for proper asset management and accountability.

ï‚· Why Other Options Are Incorrect:

A. Recorded with the original department to maximize receipts:This is incorrect because it ignores the asset's transfer and would misrepresent which department is responsible for it.

B. Recorded with the second department to minimize costs:Cost minimization is irrelevant here; the transfer should reflect the book value.

C. Retained with no change in book value to either department:While the book value doesn’t change overall, the system must reflect the transfer to the receiving department.

ï‚· References and Documents:

GAAP (Governmental Accounting Standards Board - GASB):Requires accurate fixed asset tracking to reflect departmental transfers.

GASB Statement No. 34:Discusses fixed asset tracking and reporting requirements.

Question # 28

Compliance reporting, under government auditing standards, identifies all of the following components EXCEPT

A.

areas of noncompliance.

B.

the auditor's responsibility for tests of compliance.

C.

review of major internal control cycles.

D.

the scope of the compliance testing.

Full Access

Answer:

C

Explanation:

Compliance Reporting Under Government Auditing Standards (GAS):

GAS requires auditors to assess compliance with applicable laws, regulations, contracts, and grant agreements during audits.

Compliance reporting typically includes:

Identifying areas of noncompliance.

Describing the auditor's responsibility for compliance testing.

Outlining the scope of compliance testing.

Explanation of Answer Choices:

A. Areas of noncompliance: Included in compliance reporting to highlight where the entity failed to meet requirements.

B. The auditor's responsibility for tests of compliance: GAS requires auditors to clarify their role in compliance testing.

C. Review of major internal control cycles: Correct. While internal controls may be assessed, reviewing "major internal control cycles" is not a direct component of compliance reporting.

D. The scope of the compliance testing: GAS mandates that the scope of testing be disclosed in the compliance report.

[:, GAO,Government Auditing Standards (Yellow Book)., AICPA,Compliance Reporting Guidance for Government Audits., ]

Question # 29

Cloud computing includes which of the following services?

A.

satellite-to-satellite

B.

hosted

C.

gateway transmission

D.

mainframe computing

Full Access

Answer:

B

Explanation:

Definition of Cloud Computing:

Cloud computing refers to the delivery of computing services (e.g., servers, storage, databases, networking, software) over the internet.

A common feature of cloud computing is the "hosted" service model, where applications, storage, or infrastructure are hosted and managed by a cloud service provider.

Explanation of Answer Choices:

A. Satellite-to-satellite: This involves communication between satellites, unrelated to cloud computing.

B. Hosted: Correct. Hosted services are a fundamental aspect of cloud computing, where applications or data are stored and accessed on remote servers.

C. Gateway transmission: Refers to communication gateways, unrelated to cloud computing services.

D. Mainframe computing: Mainframes are large on-premises computers, not part of the cloud model.

[:, National Institute of Standards and Technology (NIST),Cloud Computing Reference Architecture., Federal Risk and Authorization Management Program (FedRAMP),Cloud Service Providers Guidance., ]

Question # 30

The first step in investment management is to

A.

ensure all employees understand their investment options.

B.

develop a consensus among managers of the investment objectives.

C.

develop an investment policy manual.

D.

establish criteria for divesting.

Full Access

Answer:

B

Explanation:

ï‚· Investment Management Basics:

The first step in investment management is establishing theobjectivesof the investment program. This requires consensus among key stakeholders, such as managers, on what the investment goals are (e.g., risk tolerance, return expectations, liquidity needs).

Without clear objectives, subsequent steps like developing policies or selecting investments cannot be effectively carried out.

ï‚· Why Consensus Is Important:

Investment objectives must align with the organization’s mission, risk tolerance, and financial goals.

Consensus ensures that all managers are on the same page before developing specific strategies or policies.

ï‚· Why Other Options Are Incorrect:

A. Ensure employees understand their investment options:Employee understanding is not the first step; it comes later when the investment strategy is implemented.

C. Develop an investment policy manual:This happens after the objectives have been established.

D. Establish criteria for divesting:Divestment criteria are part of the investment policy and are determined later.

ï‚· References and Documents:

GAO Financial Management Guide:Highlights setting objectives as the first step in investment management.

COSO Framework for Investment Risk Management:Stresses the importance of aligning objectives before policy development.

Question # 31

To support optimal cash management vendor payment procedures, invoices with discount terms should be paid

A.

after the due date to increase cash flow.

B.

prior to the due date to improve credit rating.

C.

on the due date, unless a charge is assessed for late payment.

D.

on the discount date.

Full Access

Answer:

D

Explanation:

ï‚· Why Pay on the Discount Date?

Discount termsare offered by vendors to encourage early payment, such as "2/10, net 30" (2% discount if paid within 10 days). Paying on the discount date ensures the organization takes advantage of cost savings while still making timely payments.

This approach optimizes cash management by reducing payment obligations while maintaining good vendor relationships.

ï‚· Why Other Options Are Incorrect:

A. After the due date:Late payments can damage vendor relationships and incur penalties.

B. Prior to the due date:Paying too early does not provide additional benefits and can unnecessarily deplete cash reserves.

C. On the due date:If a discount is offered, waiting until the due date means missing the opportunity to save money.

ï‚· References and Documents:

GAO Financial Management Guide:Recommends paying invoices with discounts on the discount date to maximize cost savings.

Best Practices in Governmental Cash Management (AGA):Highlights the importance of managing vendor payments to take advantage of discounts.

Question # 32

Pay.gov is an example of

A.

a zero-balance account.

B.

a concentration system.

C.

an electronic lockbox.

D.

a data warehouse system.

Full Access

Answer:

C

Explanation:

ï‚· What Is Pay.gov?

Pay.govis anelectronic lockbox systemmanaged by the U.S. Department of the Treasury. It allows federal agencies to collect payments electronically, improving efficiency and reducing the time and cost associated with manual payment processing.

It supports online payments for taxes, fees, and other government-related obligations.

ï‚· Why Is It an Electronic Lockbox?

Pay.gov consolidates and processes payments on behalf of federal agencies, similar to how a lockbox service processes payments for private businesses.

ï‚· Why Other Options Are Incorrect:

A. Zero-balance account:This refers to a type of bank account that maintains a balance of zero by automatically transferring funds as needed, unrelated to Pay.gov’s purpose.

B. Concentration system:Refers to pooling funds from multiple accounts into one central account, not payment processing.

D. Data warehouse system:A data warehouse stores and organizes large amounts of data for analysis, unrelated to payment collection.

ï‚· References and Documents:

U.S. Treasury Pay.gov Website:Describes Pay.gov as an electronic lockbox for federal payment processing.

GAO Financial Management Systems Guide:Highlights the role of electronic lockboxes like Pay.gov in improving efficiency.

Question # 33

The Federal Credit Reform Act of 1990 prescribes a special budget treatment for direct loans and loan guarantees

that measures cash flows to and from the government using which financial analytical technique?

A.

future value

B.

net present value

C.

current value

D.

regression analysis

Full Access

Answer:

B

Explanation:

Federal Credit Reform Act of 1990:This Act established a new accounting framework for federal credit programs, such as direct loans and loan guarantees. It requires using thenet present value (NPV)method to measure the costs of loans and guarantees by discounting future cash flows (e.g., loan repayments, defaults) to their present value.

Explanation of Financial Analytical Technique:

Net Present Value (NPV): Accounts for the time value of money by discounting future cash flows to the present. It provides an accurate measure of the economic cost to the government.

Other options:

A. Future value: Focuses on future cash flows, not their present cost.

C. Current value: Not a recognized technique for analyzing long-term cash flows.

D. Regression analysis: A statistical method, unrelated to calculating loan program costs.

[:, Federal Credit Reform Act of 1990, Section 502., Congressional Budget Office (CBO),Federal Credit Program Cost Analysis., Office of Management and Budget (OMB),Circular A-11: Credit Reform Accounting., ]

Question # 34

Under government fuditing standards, auditors performing financial statement audits must

A.

design tests to assess compliance with laws, regulations, contracts and grant agreements.

B.

identify violations of laws which could be punishable by monetary penalties.

C.

identify expenditures that exceed the related obligations.

D.

design tests to detect fraud, waste and abuse.

Full Access

Answer:

A

Explanation:

Government Auditing Standards (GAS):

GAS, often referred to as theYellow Book, outlines the responsibilities of auditors conducting financial statement audits for government entities.

One core requirement is that auditors must consider compliance with applicable laws, regulations, contracts, and grant agreements that could materially affect financial statements.

Explanation of Answer Choices:

A. Design tests to assess compliance with laws, regulations, contracts, and grant agreements: Correct. This is a required component under GAS to ensure financial statements are materially accurate and comply with legal and regulatory frameworks.

B. Identify violations of laws which could be punishable by monetary penalties: Incorrect. Auditors are not required to investigate or pursue penalties but to focus on material misstatements or risks.

C. Identify expenditures that exceed the related obligations: Incorrect. While this could indicate an issue, auditors are not required to specifically test for this unless it relates to material misstatements or compliance issues.

D. Design tests to detect fraud, waste, and abuse: Incorrect. Auditors are not specifically required to detect fraud, waste, and abuse, though they should be alert to indicators.

[:, Government Accountability Office (GAO),Government Auditing Standards (Yellow Book)., Uniform Guidance (2 CFR Part 200),Audit Requirements for Federal Programs., ]