Question # 4

Your company provides a number of staff with lap-top computers, as well as pocket calculators. It capitalizes the cost of the computers and depreciates them over several years, but writes off the cost of the pocket calculators in full, against profits, in the period in which they are purchased.

The main justification for this difference in treatment is:

Question # 6

Which of the following is an example of where the historic cost convention should be applied?

Question # 9

A company uses the straight line method of depreciation for its plant and machinery. Depreciation is at a rate of 20% per annum.

A major item of machinery was purchased in 2003 at a cost of $240,000. At the time, it was estimated that the plant had an estimated useful life of five years and a residual value at the end of its useful life of $20,000.

As a result of rapid changes in technology it was decided to sell the machinery in 2006 for $80,000. It is the company's policy to charge a full year's depreciation in the year of acquisition and none in the year of disposal.

What was the profit/loss arising on the disposal of the asset?

Question # 10

Which of the following would meet the definition of a liability in accordance with the Conceptual Framework's definition?

Question # 11

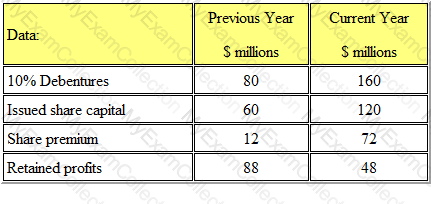

Refer to the exhibit.

A business has the following capital and long-term liabilities:

It calculates its gearing ratio as the proportion of debt to total capital.

At the end of the current year, its gearing ratio, compared with that of the previous year, is:

Question # 12

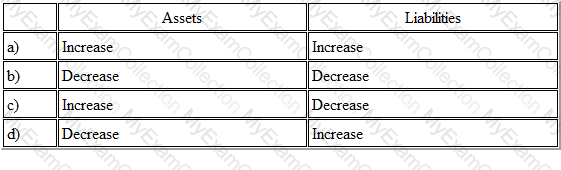

Refer to the Exhibit.

A business writes a cheque using its overdraft balance to purchase new display shelving for its showroom

Which of the following is the dual effect?

Question # 13

The purpose of the external audit is the examination of, and expression of opinion on the financial statements of an entity.

What is the purpose of internal audits?

Question # 14

Select the THREE INCORRECT statements from the following list of statements about memorandum accounts:

Question # 15

Refer to the Exhibit.

The purchase ledger control account shows a balance of £324,564, while the individual customer account balances total £328,234.

Which of the following is a possible explanation for the difference between the two?

Question # 16

A business will maintain a non-current asset register to keep a record of all non-current assets held.

Which THREE of the following are examples of information contained within the register?

Question # 17

The format of the financial statements and the disclosure notes are prescribed by accounting standards and Company Law.

Which THREE of the following are headings within the statement of financial position?

Question # 18

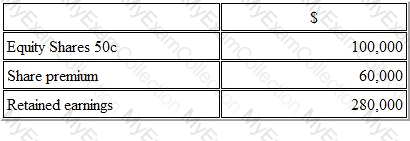

Refer to the exhibit.

A company has the following equity balances at the beginning of the year

During the year the company made a rights issue of 1 for 5 at a price of $1.50

The balance of share premium after this issue is

Question # 19

IAS 2 Inventories does not permit the use of the last in. first out (LIFO) method of valuing inventory In a time of rising prices, which of the following is a reason for this?

Question # 21

A trader commenced business with capital of $20,000. At the end of the financial year he had receivables of $10,000, payables of $6,000, inventory of $12,000, cash of $4,000 and non-current assets costing $16,000.

The profit/loss for the period was:

Question # 22

Refer to the Exhibit.

A company has the following transactions for an accounting period:

Closing inventory at the end of the period was $3,200 and gross profit was $16,400.

The opening inventory was therefore

Question # 23

Where a transaction is entered into the correct ledger accounts, but the wrong amount is used, the error is known as an error of

Question # 24

A ledger account is opened with a credit balance of $400. During the period the account is credited with $5,800 and debited with $6,500

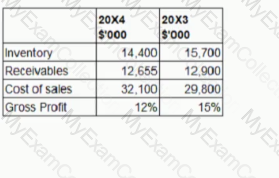

What balance will open this account in the following period?

Question # 25

Under the normal convention of accounting, assets are shown in the balance sheet at:

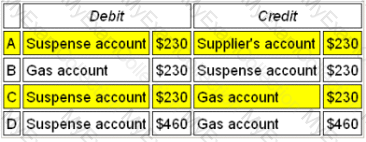

Question # 27

Refer to the exhibit.

A suspense account shows a credit balance of $230 which has arisen because of the recording of a gas bill twice in the gas account.

In order to correct the error, which one of the following journal entries is required?

The correct journal entry is

Question # 30

M Ltd owns property costing $80,000 ($50,000 for the land and $30,000 for the building).

The company's accounting policy is to depreciate buildings at the rate of 5% per annum on the straight-line basis.

After five years, what is the net book value of freehold land and building in the financial accounts of M Ltd?

Question # 31

A company which is VAT registered, has sales for the period of $28,450 (excluding VAT) and purchases (including VAT) for the period of $14,687.50.

The balance on the VAT account, assuming all items are subject to VAT at 17.5%, is:

Question # 32

In internal auditing, detection of fraud is an important objective. The auditors will best be able to detect frauds if they are knowledgeable in the most common methods of fraud.

Which THREE of the following are common methods of fraud?

Question # 33

Store Y believe customer XF will not be able to pay his £300 debt. Which ONE of the following day books should this 'bad debt' be recorded in?

Question # 35

On 31 December 20X6 GHI makes a bonus issue of 50,000 shares On this dale the nominal value of the shares is $1 and the market value is $3 GHI has a share premium account with a substantial credit balance. The share capital account is credited correctly in the nominal ledger. Which of the following statements is TRUE?

Question # 36

A non-current asset was purchased for £240000 at the beginning of Year 1, with an expected life of 7 years and a residual value of £50000. It was depreciated by 20% per annum using the reducing balance method.

At the beginning of Year 4 it was sold for £100000. The result of this was:

Question # 37

In the year ended 31 December 20X1, XYZ receives an email confirming that a major customer has gone into liquidation and will be unable to pay its suppliers.

Which of the following is the impact of adjusting for this event?

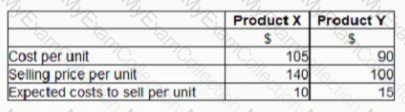

Question # 38

AB sells two products ,X and Y. The following information was available at AB’s year-end, 31 December 20X6:

At 31 December 20X6 AB held 800 units of Product X and 400 units of Product Y

What is the value that will be included in inventories in AB's statement of financial position as at 31 December 20X6?

Question # 39

Which ONE of the following deals with problems that arise with existing accounting standards?

Question # 40

Below is some information about Company TYY:

TYY offers a wholesale price for Product P of £650 per 100 quantity.

TYY offers regular customers a 35% trade discount.

On every 15th of the month, TYY offers a 15% cash discount on sales.

MPU wants to make a purchase from TTY for the first time, of900 Product Ps on the 15th of June. How much will MPU pay for this purchase?

Question # 41

A trial balance should be extracted from the ledger accounts prior to preparing the final accounts because:

Question # 42

At the beginning of the year, an organization’s non-current asset register showed a total net book value for fixed assets of £86,000. The nominal ledger showed non-current assets at cost of £120,000 and provision for depreciation of £39,000.

The disposal of a non-current asset for £10,000, at a profit of £2,000, had not been accounted for in the non-current asset register.

After correcting for this, the net book value shown in the ledger accounts would be

Question # 43

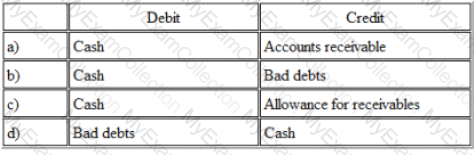

Refer to the Exhibit.

A company had previously written off one of their receivables that had been declared bankrupt. The administrators of the bankruptcy have now sent a cheque to the company for the full amount originally outstanding. The company now needs to record this receipt.

Which of the following is the correct double entry?

Question # 44

A business buys a new production line at a cost of £100,000. After using the line for one year a more advanced version of the line is marketed by the manufacturer. As a result the production line in operation has a market value of £ 50,000. The line is being depreciated straight line over five years.

The charge to the income statement for impairment of the production line will be

Question # 45

Accounting standards are used to produce the financial statements of all business entities.

Which ONE of the following best describes why accounting standards are needed?

Question # 47

Company X is a private limited oil company. Which of the following are relevant for Company X's integrated report?

Question # 48

Which of the following does not necessarily need to be true for something to be treated as an asset in an entity's statement of financial position?

Question # 49

A company uses the reduced balance method of depreciation for its company vehicles. The vehicles are depreciated at a rate of 30% per annum.

On 31 March 2003 the company purchased a number of vehicles with a total cost of $200,000. The company's year-end is 31 December and it is company policy to charge a full year's depreciation in the year of acquisition.

The carrying value of the vehicles at 31 December 2006 will be

Question # 52

The suspense account of a company was opened with a credit balance of $360 when the trial balance failed to agree.

This could have arisen because

Question # 53

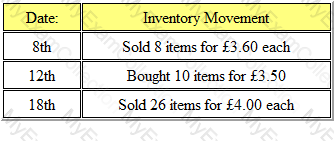

Refer to the Exhibit.

At the beginning of the month, an organization had opening inventory of 30 units of a product, valued at £3.00 each. During the month, it had inventory movements, occurring on the following dates:

Using the FIFO method of inventory valuation, the closing inventory at the end of the month was:

Give your answer to 2 decimal places.

Question # 54

A company had a gross profit margin of 40%. Sales for the period were $280,000 and opening and closing inventories were $18,000 and $16,000 respectively.

Purchases for the period were therefore

Question # 55

ABC produces accounts to the year ended 31 December annually Extracts from the most recent financial statements are.

Which of the following ratios is a liquidity ratio?

Question # 56

Comany D recently purchased an intangible asset from CompanyJFY, which was priced at £150,500, which Company D paid, along a goodwill amount that totalled 25% of the asking price.

Company D has estimated that the purchased entity will have a useful life of 35 years. Company D has decided to amortise the cost of the new asset using the straight line method.

What will the amortisation figure per annum be for Company D's new entity?

Question # 57

What will be the effect on the draft financial statements if the closing inventory figure is increased?