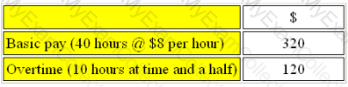

Question # 4

Refer to the exhibit.

John Brown is a machine operative in a manufacturing company. An analysis of his gross pay for the week is given below:

During the week John was idle for 6 hours due to machine breakdown and maintenance.

The total indirect labour costs included in John's gross pay was:

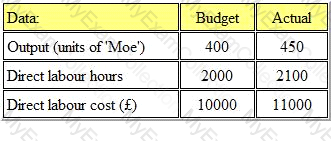

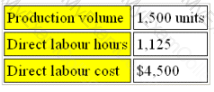

Question # 6

Refer to the exhibit.

The following details were recorded for product 'Moe' for period 2:

What was the direct labor efficiency variance?

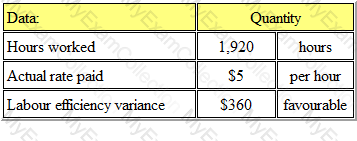

Question # 8

Refer to the exhibit.

The standard labour cost per unit of product 'B' is $24 (6 hours @ $4 per hour).

During period 5 the following details were recorded:

The output during period 5 was

Question # 9

When sales and output have passed the break-even point, the contribution per unit, for each unit then sold, becomes:

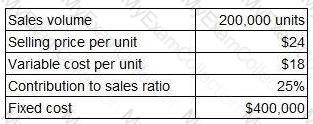

Question # 11

PQR Manufacturing Ltd. has £3,000,000 of fixed costs for the forthcoming period. The company produces a single product 'X', which has a selling price of £75 per unit and total cost of £50.

75% of the total cost represents variable costs.

How many units (to the nearest whole unit) will the organization need to produce and sell to generate a profit of £500,000?

Question # 12

It is company policy that the closing inventory of finished goods must be equal to 10% of the following month's budgeted sales. The budget sales for November and December are 50,000 and 40,000 units respectively.

The budgeted production for November will be

Question # 13

A company's output level increases but remains within the relevant range. Which ONE of the following statements is incorrect?

Question # 14

The following list contains many different types of costs for a business. However, only four of them would be considered costs centres. Which four?

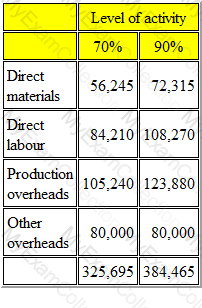

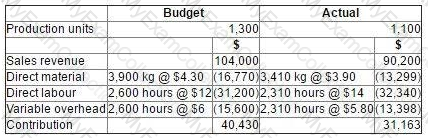

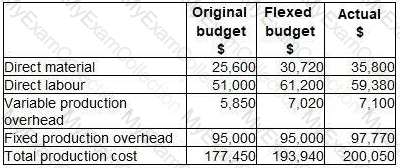

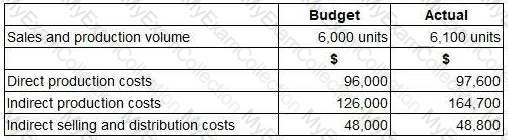

Question # 15

Refer to the exhibit.

BBB has drawn up the following flexed budgets for the year:

What would be the total budgeted costs at the 80% level of activity?

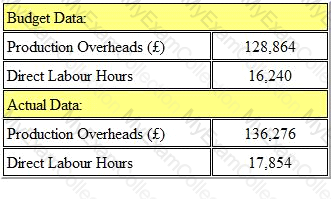

Question # 16

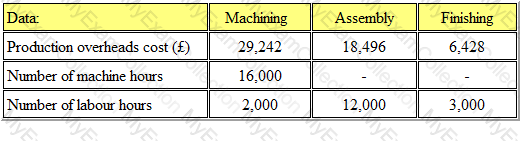

Refer to the exhibit.

The following budgetary information is available for a manufacturing company:

A particular cost unit takes 4 machine hours in the machining department and 3 labour hours in each of the assembly and finishing departments.

The overhead cost absorbed per unit is:

Give your answer to 2 decimal places.

Question # 17

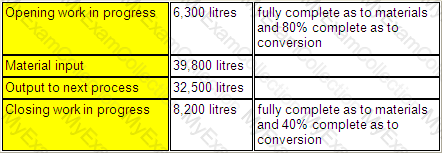

Refer to the exhibit.

A company operates a process costing system. The following data relates to Process X for the month of September.

Normal loss is 5% of input and all losses occur at the end of the process.

The number of equivalent units, using an average cost basis of valuation, was:

Conversion:

Question # 19

JB has fixed costs of $120,000 per annum. It manufactures a single product which it sells for $12 per unit. It has a profit/volume ratio of 60%.

JB’s break-even point is

Question # 20

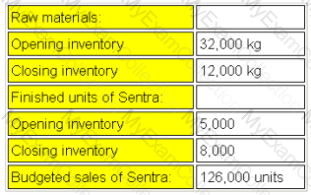

Refer to the exhibit.

The budget for product Sentra for the month of August is given below:

Each unit of Sentra requires 4kg of raw materials.

The raw materials usage budget for the month of August is:

Question # 21

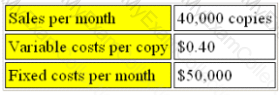

Refer to the exhibit.

ZAP publishes a monthly magazine aimed at the teenage market. It has drawn up a budget for next year as follows:

What selling price would be required for ZAP to break even?

Question # 22

A company which manufactures and sells one product has fixed costs of $80,000 per period. The selling price per unit of $25 generates a contribution/sales ratio of 40%.

How many units would need to be sold in a period to earn a profit of $10,000?

Question # 23

An organisation produces and sells a single product. The organisation’s management accountant has reported the following information for the most recent period.

Which TWO of the following statements are valid? (Choose two.)

Question # 24

A company has three production departments X, Y and Z, and one service department.

The service department’s overhead has been apportioned to the production departments in the ratio 3:2:5. As a result of this apportionment, $2,070 was given to Department Y.

What is the amount of service department overhead that would have been apportioned to Department Z? Give your answer to the nearest dollar.

Question # 25

A company’s policy is to hold closing inventory each month equal to 10% of the next month’s budgeted sales volume. The budgeted sales volumes of product Q for months 1 and 2 are 1,660 units and 2,300 units respectively.

The production budget for product Q for month 1 is:

Question # 26

A company wishes to compare the variability of its monthly sales revenue in country A with that of country B. The two countries use different currencies.

The monthly sales revenue for the last 48 months in country A (which is measured in $) has been analysed as follows.

What is the coefficient of variation of this data?

Give your answer as a percentage to one decimal place.

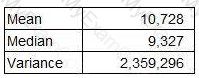

Question # 27

Data for the latest period for a company which makes and sells a single product are as follows:

There were no budgeted or actual changes in inventories during the period.

The variable overhead expenditure variance for the period was:

Question # 29

A new product requires an investment of $200,000 in machinery and working capital. The total sales volume over the product’s life will be 5,000 units. The forecast costs per unit throughout the product’s life are as follows:

The product is required to earn a return on investment of 35%.

What unit selling price needs to be achieved?

Question # 30

The staffing policy for a supermarket is to have one cashier station open for every forecasted 20 customers per hour. Cashiers are hired by the hour as and when required, and do not perform any other duties.

The cost of the cashiers in relation to the number of customers would be classified as which type of cost?

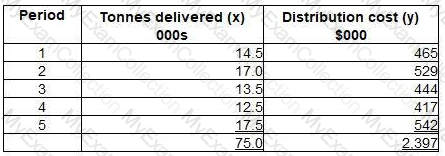

Question # 31

The following data are available for a delivery company. The table shows the number of tonnes delivered (x) and the associated distribution cist (y) in recent periods.

Further analysis of this data has determined the following:

∑xy = 36,427∑x2 = 1,144

Using least squares regression analysis, calculate the variable cost per tonne delivered. Give your answer to the nearest cent.

Question # 33

A company is appraising two projects. Both projects are for five years. Details of the two projects are as follows.

Based on the above information, which of the following statements is correct?

Question # 34

The following is an extract from a budgetary control report for the latest period:

The budget variance for prime cost is:

Question # 35

Which of the following would NOT be an appropriate performance measure for a profit centre manager?

Question # 36

A company uses full cost pricing. The unit costs for product Z are given below.

What price per unit should be charged in order to achieve a profit margin of 20%?

Give your answer to the nearest cent.

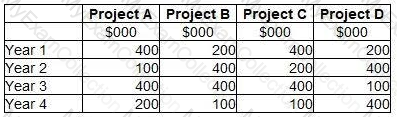

Question # 37

A management accountant has forecast the following cash inflows from four potential projects.

All four projects require the same initial investment and will last for four years. They all result in a positive net present value but only one of the projects can be undertaken.

Which project should be selected?

Question # 38

The International Federation of Accountants (IFAC) stated that it was important that “accountants in business†should understand what the drivers of stakeholder value are. Which of the following statements is valid?

Question # 39

A company uses standard absorption costing. Budgeted and actual data for the latest period are as follows.

What was the production overhead absorption rate per unit?

Question # 40

A confectionery manufacturer is considering adding a new product to the current range. Forecast data for the product are as follows.

Incremental fixed costs attributable to the new product are forecast to be $24,000 each period.

The forecast sales volume of 180 units is insufficient to achieve the target profit of $10,000 each period.

Which of the following statements is correct?

Question # 41

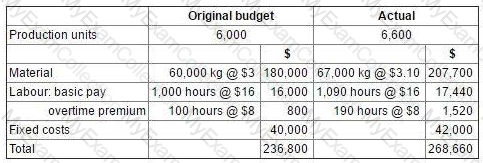

The budget and actual cost statements for the production department for the latest period were as follows.

Notes.

The 10% increase in production was required to meet unexpected additional sales demand.

The production manager is responsible for negotiating the price of materials with suppliers.

The normal working time is 900 hours per period. Any overtime worked above these 900 hours is paid at a premium of 50%.

In preparing the flexible budget for the latest period, which TWO of the following statements are correct? (Choose two.)

Question # 42

Which one of the following is NOT one of the five stated fundamental principles of CIMA's code of ethics?

Question # 43

Each finished carton of product P contains 15 litres of liquid L. During the production process there is an unavoidable loss of 20% of the liquid input. The standard price of liquid L is $2 per litre.

The standard ingredient cost for liquid L shown on the standard cost card for one carton of product P will be

Question # 45

An increase in the variable cost per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

Question # 46

SP Limited operates an absorption costing system. It uses a predetermined overhead absorption rate based on machine hours. Budgeted factory overheads for the year were £1,080,000 but actual overhead incurred was £1,046,000. Budgeted machine hours were 120,000 and actual machine hours were 119,000.

Overheads for the period were.

Question # 47

The production manager of your company has asked you to explain the methods of overhead analysis used, in particular the meaning of reciprocal servicing.

Reciprocal servicing is:

Question # 48

Which of the following statements is correct?

i. sector bodies use budgetary planning and control systems

ii. costing cannot be used by public sector bodies because they have no measurable output

iii. in public sector bodies tend to focus on cost management therefore they have no need for non-financial information

Question # 49

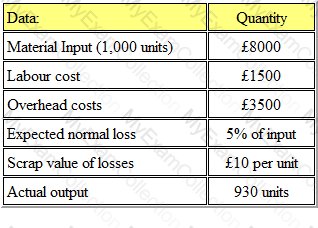

Refer to the exhibit.

The following information is available for a production process:

The cost per unit of good output is:

Give your answer to 2 decimal places.

Question # 50

Which ONE of the following would be the LEAST effective performance indicator for a distribution manager who is responsible for controlling the cost of the transport fleet?

Question # 51

Refer to the exhibit.

The budget for ORG for the month of September contained the following data:

During the month the actual number of units produced was 1,550. The management accounts showed a direct labour rate variance of $200 adverse and direct labour efficiency variance of $150 adverse.

The actual direct labour hours in the month was:

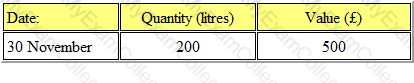

Question # 52

Refer to the Exhibit.

Fabex Ltd manufactures a household detergent called "Clear". The standard data for one of the chemicals used in production (chemical XTC) is as follows:

(a) 50 litres used per 100 litres of 'Clear' produced

(b) Budgeted monthly production is 1000 litres of 'Clear'.

The closing inventory of chemical XTC for November valued at standard price was as follows:

Actual results for the period during December were as follows:

(a) 500 litres of chemical XTC was purchased for £1300.

(b) 550 litres of chemical XTC was used.

(c) 900 litres of 'Clear' was produced.

It is company policy to extract the material price variance at the time of purchase.

What is the total direct material price variance (to the nearest whole number)?

Question # 53

Refer to the exhibit.

The following data relates to Department A within a business unit.

The overhead absorption rate per direct labour hour for Department A is:

Give your answer to 2 decimal places.

Question # 54

Each unit of product GM requires 4 labour hours to be produced. 25% of the units will be completed during overtime hours.

Sales of 24,000 units are planned and finished goods inventory is budgeted to rise by 2,000 units.

If the wage rate is £6 per hour and the overtime premium is 50%, what is the budgeted labour cost?

Question # 55

A company uses an integrated accounting system.

The accounting entries for the sale of goods on credit would bE.

Question # 56

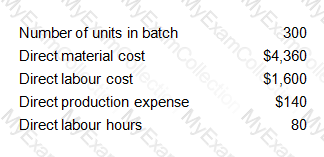

Refer to the Exhibit.

A company operates a batch costing system.

Production overhead costs are absorbed into the cost of batches using a direct labour hour rate. Other overhead costs are absorbed at a rate of 20% of total production cost. The company adds a mark-up of 10% to total cost in order to derive its selling prices.

Budgeted production overheads for the period are $44,000 and the budgeted level of activity is 8,800 direct labour hours.

The following data are available for batch number 309:

The required selling price per unit (to two decimal places) is:

Question # 57

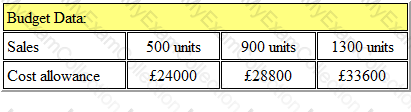

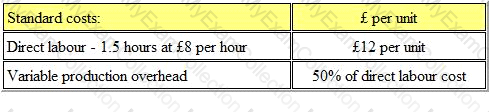

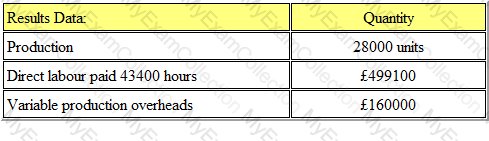

Refer to the exhibit.

Budget information for 'Crome Ltd' is as follows:

The budgeted cost allowance for the sale of 1000 units would be:

Question # 58

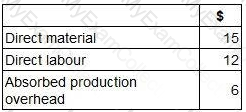

Refer to the Exhibit.

AM Ltd. makes and sells a single product for which the standard cost information is as follows:

- Budgeted production for the period is 30000 units.

- The actual results for the period were as follows:

What is the variable overhead expenditure variance?