Question # 4

The unexpected loss for a credit portfolio at a given VaR estimate is defined as:

Question # 5

When modeling operational risk using separate distributions for loss frequency and loss severity, which of the following is true?

Question # 6

Which of the following are elements of 'group risk':

I. Market risk

II. Intra-group exposures

III. Reputational contagion

IV. Complex group structures

Question # 7

The key difference between 'top down models' and 'bottom up models' for operational risk assessment is:

Question # 8

When pricing credit risk for an exposure, which of the following is a better measure than the others:

Question # 9

An operational loss severity distribution is estimated using 4 data points from a scenario. The management institutes additional controls to reduce the severity of the loss if the risk is realized, and as a result the estimated losses from a 1-in-10-year losses are halved. The 1-in-100 loss estimate however remains the same. What would be the impact on the 99.9th percentile capital required for this risk as a result of the improvement in controls?

Question # 10

Which of the following is a valid approach to determining the magnitude of a shock for a given risk factor as part of a historical stress testing exercise?

I. Determine the maximum peak-to-trough change in the risk factor over the defined period of the historical event

II. Determine the minimum peak-to-trough change in the risk factor over the defined period of the historical event

III. Determine the total change in the risk factor between the start date and the finish date of the event regardless of peaks and troughs in between

IV. Determine the maximum single day change in the risk factor and multiply by the number of days covered by the stress event

Question # 11

Under the standardized approach to calculating operational risk capital under Basel II, negative regulatory capital charges for any of the business units:

Question # 12

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

Question # 13

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds over a one year horizon are 0.03 and 0.08 respectively. If the default correlation is zero, what is the one year expected loss on this portfolio?

Question # 14

Which of the following is not a consideration in determining the liquidity needs of a firm (as opposed to determining the time horizon for liquidity risk)?

Question # 15

Which of the below are a way to classify risk governance structures:

A Reactive, Preventative and Active

B. Committee based, regulation based and board mandated

C. Top-down and Bottom-up

D. Active and Passive

Question # 16

If A and B be two uncorrelated securities, VaR(A) and VaR(B) be their values-at-risk, then which of the following is true for a portfolio that includes A and B in any proportion. Assume the prices of A and B are log-normally distributed.

Question # 18

An investor holds a bond portfolio with three bonds with a modified duration of 5, 10 and 12 years respectively. The bonds are currently valued at $100, $120 and $150. If the daily volatility of interest rates is 2%, what is the 1-day VaR of the portfolio at a 95% confidence level?

Question # 19

When combining separate bottom up estimates of market, credit and operational risk measures, a most conservative economic capital estimate results from which of the following assumptions:

Question # 20

Who has the ultimate responsibility for the overall stress testing programme of an institution?

Question # 21

Which of the following describes rating transition matrices published by credit rating firms:

Question # 22

Which of the following contributed to the systemic failure during the credit crisis that began in 2007?

Question # 23

When compared to a low severity high frequency risk, the operational risk capital requirement for a medium severity medium frequency risk is likely to be:

Question # 24

According to the Basel framework, shareholders' equity and reserves are considered a part of:

Question # 25

A risk analyst peforming PCA wishes to explain 80% of the variance. The first orthogonal factor has a volatility of 100, and the second 40, and the third 30. Assume there are no other factors. Which of the factors will be included in the final analysis?

Question # 26

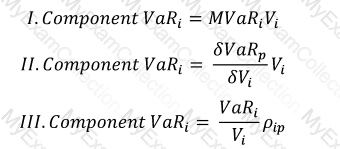

Which of the following formulae correctly describes Component VaR. (p refers to the portfolio, and i is the i-th constituent of the portfolio. MVaR means Marginal VaR, and other symbols have their usual meanings.)

Question # 27

Which of the following carry greater counterparty risk: a forward contract on a 10 year note, or a commercial paper carrying a AA credit rating with identical maturity and notional?

Question # 28

Which of the following is a most complete measure of the liquidity gap facing a firm?

Question # 29

Which of the following is not a permitted approach under Basel II for calculating operational risk capital

Question # 31

Which of the following is a measure of the level of capital that an institution needs to hold in order to maintain a desired credit rating?

Question # 32

Which of the following is not an event of default covered in the ISDA Master Agreement?

I. failure to pay or deliver

II. credit support default

III. merger without assumption

IV. Bankruptcy

Question # 33

The VaR of a portfolio at the 99% confidence level is $250,000 when mean return is assumed to be zero. If the assumption of zero returns is changed to an assumption of returns of $10,000, what is the revised VaR?

Question # 34

Which of the following credit risk models considers debt as including a put option on the firm's assets to assess credit risk?

Question # 35

Which of the following statements are true:

I. Credit risk and counterparty risk are synonymous

II. Counterparty risk is the contingent risk from a counterparty's default in derivative transactions

III. Counterparty risk is the risk of a loan default or the risk from moneys lent directly

IV. The exposure at default is difficult to estimate for credit risk as it depends upon market movements

Question # 36

Which of the following are valid approaches to calculating potential future exposure (PFE) for counterparty risk:

I. Add a percentage of the notional to the mark-to-market value

II. Monte Carlo simulation

III. Maximum Likelihood Estimation

IV. Parametric Estimation

Question # 37

Which of the following are attributes of a robust stress testing programme at a bank?

Question # 38

Which of the following assumptions underlie the 'square root of time' rule used for computing VaR estimates over different time horizons?

I. the portfolio is static from day to day

II. asset returns are independent and identically distributed (i.i.d.)

III. volatility is constant over time

IV. no serial correlation in the forward projection of volatility

V. negative serial correlations exist in the time series of returns

VI. returns data display volatility clustering

Question # 39

If the returns of an asset display a strong tendency for mean reversion, what is the relationship between annualized volatility calculated based on daily versus weekly volatilities (using the square root of time rule)?

Question # 40

In January, a bank buys a basket of mortgages with a view to securitize them by April. Due to an unexpected lack of investors in the securitization market, it is unable to do so and is left with the exposure to the mortgages on its books. This is an example of:

Question # 41

Which of the following represent the parameters that define a VaR estimate?

Question # 42

Which of the following is not one of the 'three pillars' specified in the Basel accord:

Question # 43

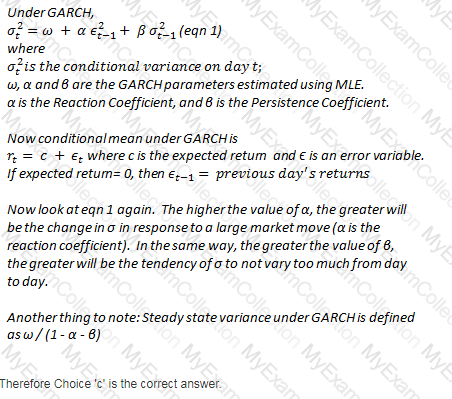

As the persistence parameter under GARCH is lowered, which of the following would be true:

Question # 44

A risk analyst attempting to model the tail of a loss distribution using EVT divides the available dataset into blocks of data, and picks the maximum of each block as a data point to consider.

Which approach is the risk analyst using?

Question # 45

CreditRisk+, the actuarial model for calculating portfolio credit risk, is based upon:

Question # 46

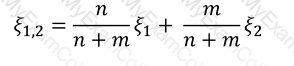

For a hypotherical UoM, the number of losses in two non-overlapping datasets is 24 and 32 respectively. The Pareto tail parameters for the two datasets calculated using the maximum likelihood estimation method are 2 and 3. What is an estimate of the tail parameter of the combined dataset?

Question # 47

Which of the following are true:

I. Monte Carlo estimates of VaR can be expected to be identical or very close to those obtained using analytical methods if both are based on the same parameters.

II. Non-normality of returns does not pose a problem if we use Monte Carlo simulations based upon parameters and a distribution assumed to be normal.

III. Historical VaR estimates do not require any distribution assumptions.

IV. Historical simulations by definition limit VaR estimation only to the range of possibilities that have already occurred.

Question # 48

A stock that follows the Weiner process has its future price determined by:

Question # 49

Which of the following statements are true:

I. The three pillars under Basel II are market risk, credit risk and operational risk.

II. Basel II is an improvement over Basel I by increasing the risk sensitivity of the minimum capital requirements.

III. Basel II encourages disclosure of capital levels and risks

Question # 50

Which of the following are valid approaches for extreme value analysis given a dataset:

I. The Block Maxima approach

II. Least squares approach

III. Maximum likelihood approach

IV. Peak-over-thresholds approach

Question # 52

An assumption of normality when returns data have fat tails leads to:

I. underestimation of VaR at high confidence levels

II. overestimation of VaR at low confidence levels

III. overestimation of VaR at high confidence levels

IV. underestimation of VaR at low confidence levels

Question # 53

The loss severity distribution for operational risk loss events is generally modeled by which of the following distributions:

I. the lognormal distribution

II. The gamma density function

III. Generalized hyperbolic distributions

IV. Lognormal mixtures

Question # 54

All else remaining the same, an increase in the joint probability of default between two obligors causes the default correlation between the two to: